Inside Private Credit: How Afranga Structures Returns and Risks

High yields in private credit often look straightforward — the underlying structure usually isn’t.

From an investor’s perspective, the key questions go beyond returns: How are loans structured? Who stands behind them? What happens if payments are delayed? And how much protection does regulation really provide?

Afranga offers one approach to answering these questions through a direct lending model, where investors fund loan originators and receive monthly repayments, without intermediary structures. Each investment is supported by standardized disclosures under the European Crowdfunding Service Providers Regulation, while tools like SaveSmart aim to simplify access without turning the investment into a “black box.”

At the same time, returns depend on credit performance, recovery processes, and the financial strength of originators — not guarantees.

In this interview, CEO Svetlin Sabev explains how Afranga selects originators, structures repayments, manages delays, and what investors should realistically expect in terms of risk, liquidity, and control.

Platform Positioning and Growth

Afranga focuses on building a more direct and structured approach to private credit investing, aiming to reduce complexity and improve transparency for retail investors.

According to CEO Svetlin Sabev, the company aims to simplify access to this asset class.

“Today Afranga is positioned as a digital bridge connecting retail capital with high-yield credit opportunities.”

The platform targets self-directed investors looking for transparent, technology-driven investment options within the EU.

Since launch, Afranga has shown steady growth. The platform reports over €30 million invested and a community of more than 5,000 active investors. It has also expanded its operational footprint across multiple countries and received industry recognition, including an award at the Forbes Innovation Awards 2025.

Business Model and Investment Structure

Afranga operates with a direct investment model, where investors fund loans to project owners without intermediated structures commonly seen in traditional P2P platforms.

“By enabling investors to fund loans directly to project owners, we eliminate the loan transfer agreements that often obscure investor rights in legacy systems.”

This structure is designed to provide clearer legal relationships and reduce structural complexity. Each investment is accompanied by a Key Investment Information Sheet (KIIS), offering detailed insights into risk and return.

The platform also emphasizes a “zero fees for investors” approach. In practice, this means that investors are not charged platform fees, and returns are not reduced by hidden costs.

Instead, investors are expected to focus on portfolio-level factors such as credit risk and capital allocation.

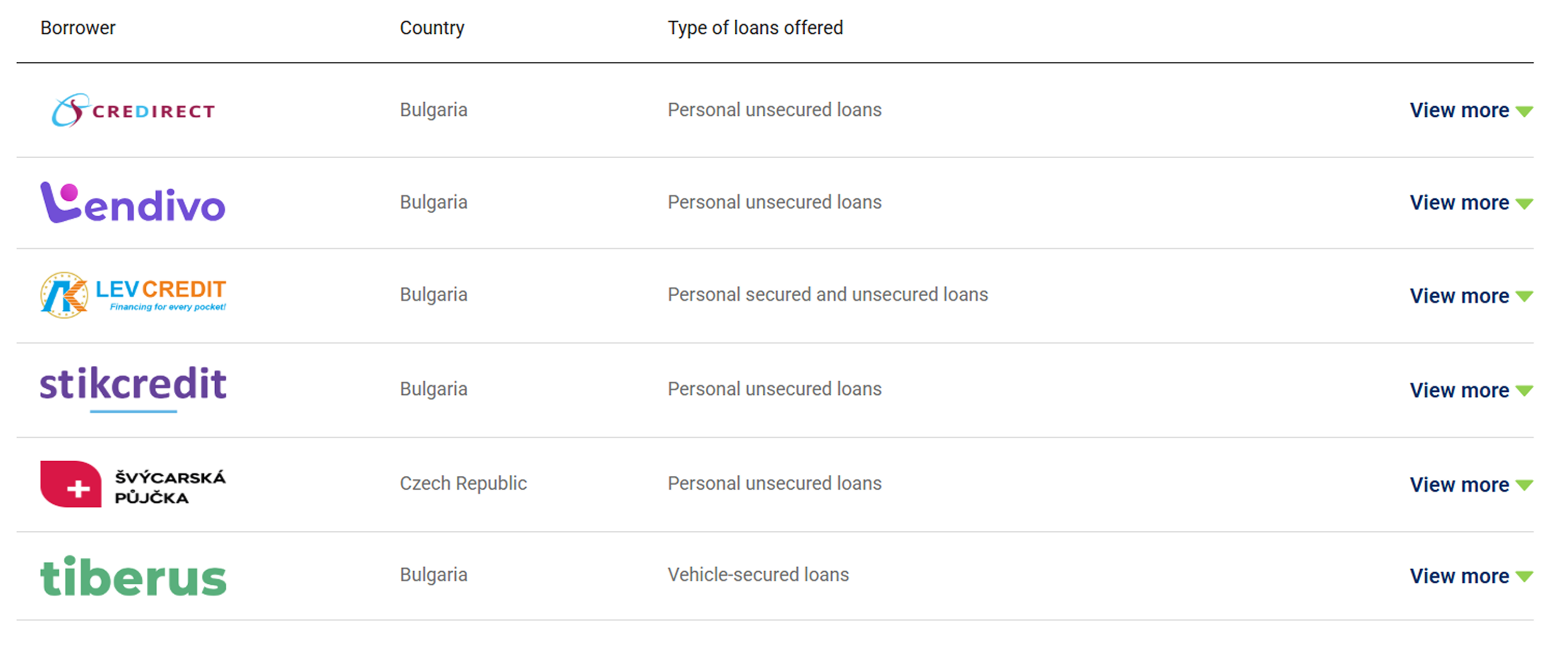

Risk Management and Loan Originators

Risk management is a central part of Afranga’s model, particularly when it comes to selecting and monitoring loan originators — the entities ultimately responsible for generating returns for investors.

The platform follows a data-driven due diligence process that goes beyond standard checks.

“Our process is data-centric rather than paper-centric.”

At the onboarding stage, Afranga evaluates originators across several key dimensions:

- Financial health: profit and loss, balance sheet, cash flow

- Core metrics: solvency, profitability, equity ratios

- Track record: performance across different market cycles

- Business fundamentals: ownership structure, management quality, growth strategy

In addition to financial analysis, the platform also focuses on how originators assess risk internally. This includes:

- use of scoring algorithms and underwriting models

- level of automation in credit decisions

- ability to generate predictive, data-driven risk assessments

The goal is to ensure that risk assessment is not only robust but also scalable and consistent. The evaluation further extends to governance and compliance, including internal controls and AML procedures, in line with the European Crowdfunding Service Providers Regulation.

Ongoing Monitoring

Once onboarded, originators are continuously monitored using a set of performance indicators:

- Portfolio-at-risk (PAR)

- Collection efficiency

- Vintage performance analysis

These metrics help identify early signs of deterioration before they become systemic issues.

“If our monitoring systems detect a shift in an originator’s risk profile or a cooling in their local economy, we have the capability to adjust or cap the volume of new loans/ projects they can list on Afranga.”

This allows Afranga to react dynamically — for example, by limiting or pausing new listings from specific originators if risk levels increase.

Handling Delays and Defaults

So far, Afranga reports that it has not experienced originator defaults. However, it has established a structured framework to manage potential issues.

If a borrower misses a payment, the platform then follows a recovery approach:

- Late interest accrues immediately as compensation for the delay

- The situation is assessed, followed by potential restructuring of the repayment plan

- If unresolved, legal proceedings may be initiated

Throughout this process, Afranga coordinates communication and recovery efforts.

Importantly, due to the direct lending structure, investors hold legal claims against the borrower.

“Each direct loan is backed by the originator’s full corporate assets.”

This means that, in case of default, recovery is not limited to a single asset but can extend to the broader balance sheet of the originator — although outcomes ultimately depend on the financial condition of the borrower.

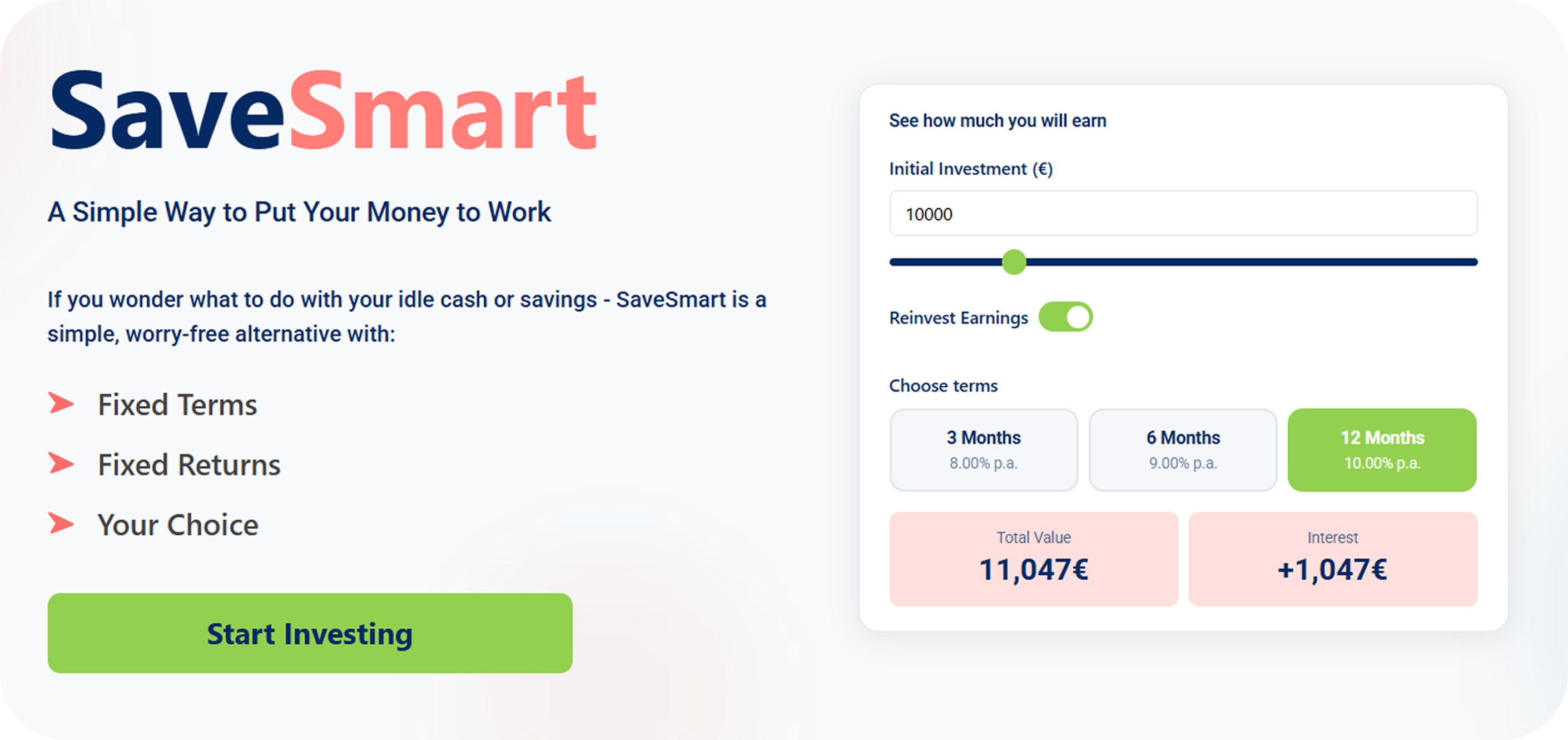

Investor Experience and SaveSmart

Afranga’s investor experience is built around simplicity and transparency. The platform offers digital onboarding, streamlined investment selection, and a dashboard that tracks performance and accrued interest.

Within this ecosystem, SaveSmart — Afranga’s investment tool — is positioned as a simplified entry point into private credit investing.

“SaveSmart is built on the principle of direct private lending. When you invest, you are entering into ad legally binding loan agreement directly with a vetted Loan Originator.”

Unlike traditional savings accounts, SaveSmart is not a deposit product but a direct loan investment with associated risks. While it is not covered by deposit guarantee schemes, it operates under the European Crowdfunding Service Providers Regulation, which provides standardized protections such as the Key Investment Information Sheet (KIIS).

Returns are generated through lending to vetted loan originators, with performance linked to their financial strength and repayment capacity.

From a portfolio perspective, SaveSmart sits between low-risk savings products and more complex investment strategies.

“It is designed for those who find traditional savings accounts too stagnant and active crowdfunding investing too time-consuming.”

However, it does not provide the same level of capital protection as traditional savings products, requiring investors to consider both credit risk and liquidity constraints.

ECSP Regulation and Investor Protection

Afranga operates under the European Crowdfunding Service Providers Regulation, which introduces a unified set of investor protection standards across the EU.

From an investor’s perspective, the framework provides several tangible safeguards:

- Key Investment Information Sheet (KIIS) — a standardized document that outlines the risks, structure, and expected returns of each investment in a clear and comparable format

- Appropriateness assessment and loss simulation — tools designed to help investors understand whether crowdfunding investments match their financial situation and risk tolerance

- 4-day reflection period — a cooling-off window during which investors can withdraw from an investment without penalty

- Segregation of funds via licensed payment providers — investor funds are held by regulated third parties, ensuring they remain separate from the platform’s operational accounts

In addition, the regulation requires platforms to maintain operational resilience, including business continuity plans and transparent reporting standards.

At the same time, regulation does not eliminate investment risk.

“While we provide the tools to evaluate every loan, the risk of a project owner defaulting or a Loan Originator facing financial distress cannot be regulated away.”

In this sense, ECSP improves transparency and structure, but investment outcomes still depend on the quality of the underlying assets, leaving investors exposed to credit and liquidity risks and responsible for making their own investment decisions.

Transparency, Returns, and Liquidity

Afranga positions transparency as a core feature rather than a reporting obligation, giving investors continuous visibility into their portfolios.

Investors have access to:

- Real-time loan status updates

- Platform-wide performance statistics

- Standardized reporting on delays and defaults

In terms of performance, Afranga positions its offering around double-digit returns, reflecting the nature of private credit investing.

“The trade-off for these superior returns is capital lock-up.”

In practice, this means that while returns may exceed those of traditional savings products or bonds, investors should be prepared to commit their capital for a defined period, with limited liquidity compared to public markets.

This makes liquidity an important factor to consider when investing through the platform.

To address this, Afranga is working on improving flexibility. In the near term, the platform plans to introduce partial withdrawal options for SaveSmart users, allowing limited early access to funds.Further developments, including the potential launch of a secondary market, are also under consideration as part of a broader effort to enhance liquidity over time.

Market Outlook and Strategy

As the European crowdfunding market continues to mature, platforms are increasingly shifting from niche solutions toward more structured, scalable investment ecosystems.

In this environment, Afranga sees regulation not just as a requirement, but as a foundation for long-term growth.

“Afranga is using ECSP to scale from a niche platform to a trusted European financial powerhouse.”

Looking ahead, the company’s priorities focus on strengthening both its product and overall investor experience:

- Improving platform usability

- Launching a mobile version

- Strengthening brand identity

- Exploring secondary market functionality

These developments are aimed at making the platform more accessible while gradually expanding its functionality for a broader range of investors.

Final Perspective

Afranga reflects a broader shift in how private credit is becoming accessible to retail investors across Europe — moving from a niche, institution-driven space toward more transparent and structured digital platforms.

Its model brings together direct lending, regulatory alignment under the European Crowdfunding Service Providers Regulation, and a simplified user experience designed to lower the barrier to entry.

At the same time, the fundamentals of private credit remain unchanged. Higher return potential comes with trade-offs — particularly in terms of credit risk and liquidity — requiring a clear understanding from investors.

In this context, Afranga illustrates how a modern crowdlending platform operates in today’s market — not by reducing complexity, but by structuring it more clearly through direct lending models, ECSP-driven transparency, and simplified tools like SaveSmart, making private credit more accessible without obscuring its underlying mechanics.